[fusion_builder_container hundred_percent=”no” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” overlay_color=”” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” padding_top=”” padding_bottom=”” padding_left=”” padding_right=””][fusion_builder_row][fusion_builder_column type=”1_1″ layout=”1_1″ background_position=”left top” background_color=”” border_size=”” border_color=”” border_style=”solid” border_position=”all” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” center_content=”no” last=”no” min_height=”” hover_type=”none” link=””][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” class=”” id=””]When starting an e-commerce business, one of the most important decisions you face is selecting the payment processor.

Be sure to choose a reliable payment processing solution that will fit your business model, all without smothering you with fees.

Because there are so many payment solutions options in Canada, picking the right one can prove to be a real headscratcher.

To help set you straight, we’ve prepared this in-depth guide to walk you through choosing the best payment processor for your e-commerce.

Table of Contents

Popular payment processors in Canada – Features, Rates and Fees Comparison

To kick things off, let’s go over the most popular e-commerce payment processors in Canada along with their features, rates and fees.

Stripe

Starting with the simplest, Stripe is a very popular payment processor for e-commerce businesses. Straight-forward fees and well-rounded features make it the go-to solution for small businesses and startups.

Stripe’s PAY AS YOU GO plan only charges when you make a sale. Each successful transaction will cost you a flat 2.9% + $0.3 per transaction.

You only pay for what you use. That means no setup, monthly or any other hidden fees.

No contracts or monthly fees are key when you’re just starting out. This helps keep overheads at a minimum, a clear benefit for new businesses.

Simplicity is another great advantage; with Stripe’s transparent and straightforward pricing you can easily predict and control your costs.

Stripe also comes with a wide range of options and features for all your e-commerce needs. This includes a full stack of payment methods (accepting Mastercard, Visa, Amex, etc.), as well as customizable checkout forms that blend in perfectly with your site’s design.

It’s easy to get started with Stripe, there is no approval period or verification process, so you can set up shop and start making sales pretty much immediately.

In general, anyone can start accepting online payments within a few minutes (literally) using Stripe.

And this is a huge advantage when you’re starting a new e-commerce business.

Stripe breakdown:

- Domestic (Canada) payments 2.9% + $0.3 per transaction

- International payments cost additional 0.6% per transaction (+2% conversion rate if necessary)

- No setup, monthly or hidden fees

- Accept payments from credit/debit cards, local payment methods (Interac) and digital wallets (i.e. ApplePay)

- Fixed rates across all payment methods

- Rates are negotiable (down to 2.2%) after processing over $100K/month

- Chargebacks $15-$0 depending on who wins the dispute

PayPal

PayPal is probably the most well-known payment service that allows you to pay, send and accept payments online. For this guide, let’s focus on the “accepting payments” part.

For e-commerce, PayPal offers two options: PayPal Standard and PayPal Pro.

PayPal Standard

The standard service allows you to accept payments for your online store both from credit/debit cards and PayPal funds.

It’s completely free of overheads, costing you only the flat rate fee of 2.9% + $0.3 per transaction.

Similar to Stripe, you only pay when you make a sale. No monthly, setup or any other additional fees, which makes it the PayPal’s simplest option.

However, this does come with a major caveat.

PayPal Standard doesn’t allow customers to complete the checkout on your own site (aka on-site checkout). Instead, when your customers are ready to pay, they’ll be redirected to a special checkout page hosted on PayPal.

This can have a negative impact on your conversion rate. Any disturbance during the checkout stage (like redirecting to another site) may discourage shoppers from completing the order, leading to a loss in conversion/sale.

The main advantages of PayPal Standard are that it’s simple and it doesn’t charge any additional fees other than the transaction fee. Many WordPress and WooCommerce scripts also support Paypal by default.

Here’s a breakdown of PayPal Standard:

- Domestic (Canada) payments 2.9% + $0.3 per transaction

- Payments from the US 3.7% + $0.3 per transaction

- International payments (outside CA and the US) 3.9% + a fixed fee depending on the country

- No startup costs, no termination fee, no monthly fees

- Includes processing all cards as well as PayPal payments

- Off-site checkout

Despite its shortcomings, PayPal Standard does make perfect sense in certain scenarios. More on this in the next chapter.

PayPal Pro

On the other side, you have PayPal Pro which is a fully customizable processing solution to accept payments directly on your site.

And that’s PayPal Pro’s main standout feature compared to Standard; your customers can pay without leaving your site for a seamless purchasing experience.

Each sale will set you back 2.9% + $0.3 per transaction (domestic), same as Standard. However, the Pro plan also charges a $35 CAD monthly fee (+HST).

PayPal Pro also includes a few more features that separate it from the standard plan.

You can accept payments over the phone with PayPal’s Virtual Terminal as well as collect recurring payments. If you want to automate your subscription (recurring) billing, this add-on will cost you an additional $10 per month.

Finally, it’s also good to know that with PayPalPro your rates are negotiable after you process a certain volume (it’s best to contact your account rep). You could potentially talk terms to get lower rates for each card type.

In our experience, we’ve seen MasterCard and Visa rates negotiated down to just 1.6% and AMEX to 3.1%, but this will vary from case to case.

Your merchant account scales with you, so you can lower your rates and get better terms in the future.

PayPal Pro breakdown:

- Domestic payments (Canada) 2.9% + $0.3 per transaction

- Payments from the US 3.7% + $0.3 per transaction

- International payments (outside CA and the US) 3.9% + fixed fee depending on the country

- 3.5% for AMEX for all countries

- Additional $35 per month + HST

- Includes everything from PayPal Standard with on-site checkout

- Customizable payment forms

- Rates are negotiable after you reach certain volume (depending on your business etc. – talk to your account manager/rep)

- Virtual Terminal, which is a simplified POS system you can use for accepting payments with your phone

- Chargeback fees depending on the currency (for CAD it’s $20)

- Refund fee $0.3

Bambora

Bambora (formerly Beanstream) is vastly popular among small and medium e-comms in Canada. Its month-to-month contract and competitive pricing make it an attractive payment solution for businesses of any size.

Pricing comes in two main forms – Blended and Interchange Plus.

Bambora Blended Pricing

Bambora’s Blended pricing is suitable for new and small businesses. No matter the type of card, each sale will cost you a fixed 2.8% + $0.3.

On top of that, Bambora also charges a $25 monthly fee as well as a $49 one-time setup fee.

The main benefit of this model is its predictability, so you’ll have an easier time understanding and controlling your costs.

Bambora deals strictly with online payments and their in-house gateway can be paired with a merchant account from another processor if you need it.

Plus, you have full control over your checkout experience with plenty of options for your customers (credit and debit cards, digital wallets and direct payment – EFT and ACH).

One big drawback of Bambora is that you can’t just start using it whenever you want. You need to get in touch with their sales reps and wait to get approved. And sometimes you might not get approved at all because they may decide not to support your business for whatever reason.

BamboraBlended Rate breakdown:

- 2.8% + $0.3 per transaction

- Flat fee for all transactions (no matter the brand, type or country)

- Additional $25 monthly fee and a $49setup fee

- Chargeback fee $20

- No hidden fees

- Month to month contract

- No cancellation fee

- PCI Compliant (no fees)

Bambora Interchange + Pricing

If you’re processing large volumes (over $5 million annually), Bambora offers Interchange Plus pricing model.

Each transaction cost will be different. This means the cost for each sale is calculated by adding:

- Interchange fee set by the card brand (i.e. VISA, MasterCard, AMEX).

- Scheme fee – additional fees set by the card brands depending on the card type, issuing bank, country, etc.

- Processor fee which is charged by Bambora.

For example, MasterCard Standard card would cost:

1.65% (set by MC) + 0.12% (Scheme/Assessment fee) +Bamborafee (depending on volume)

Generally, the more premium a card is, the more expensive its interchange fee will be.

American Express has far fewer assessment fees. With American Express, you are charged 1.6% + $0.1 for internet orders and an additional 0.1356% network fee, on top of the Bambora transaction fee.

Interchange plus pricing model is more suitable for larger companies who want granular control over their processing costs. You get transparent reporting for individual transactions and can lower costs by optimizing how payments are routed.

This makes it suitable for B2B e-commerce since AMEX transactions will cost you far less than with either PayPal or Stripe.

Bambora Interchange Plus breakdown:

- Interchange Plus Rate = Interchange rate (%) + Fee set by the Card Brand ($) + Bambora fee ($)

- Flexible, depending on the Card Brand, issuing bank, type of card, etc.

- Bambora markup (fee) depending on your processing volume

- Need to be processing over $5 million per year to be eligible for this pricing model

Moneris

Moneris is on the opposite side of the spectrum from Stripe, PayPal. It’s more of a traditional payment processor that services e-commerce as well as brick-and-mortar stores.

If you’re running a physical store, Moneris has an all-round solution with card processing and POS equipment.

For e-commerce, Moneris provides a proprietary Moneris Gateway. This can come as a hosted payment page or integrated directly into your website.

Moneris Gateway includes all the standard features you would expect, including a Vault to store recurring customer data, shopping cart integration, tokenization for security and PCI compliance.

Moneris’ pricing model is entirely quote-based. That means each business will get different terms and pricing depending on the size, industry, processing volume, etc.

Similar to Bambora (Interchange Plus), your processing cost will vary wildly from transaction to transaction depending on the card type, issuing bank, country, etc.

For example, some quotes we got contained the following terms:

- Monthly fee $39.95 +HST

- No contract

- Transaction fees for MasterCard / VISA @ 1.6% + $0.05

- Transaction fees using AMEX @ 2.0% + $0.05

- Chargeback fee $25

- Charge extra of $10 for a virtual terminal (which you can use to manually input credit card details into the system)

- One-time setup fee (non-refundable) @ $150 +HST

Just remember to take this example with a grain of salt as quotes will be different for each business.

Moneris is a great solution if you have very large processing volumes and can anticipate where your transactions will come from.

This can result in much lower per-transaction fees, (typically lower than Stripe and PayPal) especially for B2B sellers who deal mostly with AMEX.

It’s very important to note that in some cases Moneris also locks clients with a 3-year contract. And their service may come with many additional/hidden fees such as:

- monthly fees

- setup fees

- equipment rental

- PCI compliance fees

- early cancellation fees

- deposit fees, etc.

Some of these fees can be waived to keep your costs down, but you have to be a strong negotiator and know what you’re doing.

To put it in Forest Gump’s words, Moneris is like a box of chocolates. You never know what you’re gonna get.

If you want to try Moneris it’s best you contact their sales and request a quote. It will take some time before you get a reply, and then some to get approved and finalize the setup on your e-store.

Also, you may experience the same problem as with Bambora. Moneris might decide not to support your e-commerce for reasons unknown.

Despite very competitive rates, Moneris may not be the best fit if you’re just starting with e-commerce.

It works best for more established businesses with massive transaction volumes. Also, if you’re running both an e-comm and a physical store, Moneris is right for you.

B2B businesses will also benefit from low AMEX rates.

Moneris payment processor breakdown:

- Transaction rates are different for each card brand. They are negotiable and determined for each client.

- Setup fee (~$150 +HST)

- Monthly fee (~$40 +HST)

- Many additional fees such as compliance fee, deposit fee, etc. (some can be waived through negotiation)

- Chargeback fee (~$20)

- Minimum processing volume (~$20/month)

- Virtual terminal requires an additional $10

- POS terminals and equipment range from $20-90/month

Stripe vs PayPal vs Bambora vs Moneris Cost Comparison

| Stripe | PayPal Standard | PayPal Pro | Bambora | Moneris | |

|---|---|---|---|---|---|

| Transaction fee | Flat 2.9% + $0.3 | Flat 2.9% + $0.3 | Flat 2.9% + $0.3 | Flat 2.8% + $0.3 | Quote-Based(~ 1.6% + $0.05) |

| Negotiable rates | Yes Over $100K/month | No | Yes | Yes Over $5million/year | Yes |

| Monthly fee | None | None | $35 (+HST) | $25 | Yes, varies (~$40 +HST) |

| Setup fee | None | None | None | $49 | Yes, varies (~$150 +HST) |

| Contract | No | No | No | Month to month | Quote-Based |

| Cancellation fee | No | No | No | No | Yes |

| Chargeback fee | $15-0 | Varies ($20 for Canadian) | Varies ($20 for Canadian) | $20 | ~$25 |

| Hidden fees | / | / | / | / | Yes |

| Stripe | |

|---|---|

| Transaction fee | Flat 2.9% + $0.3 |

| Negotiable rates | Yes Over $100K/month |

| Monthly fee | None |

| Setup fee | None |

| Contract | No |

| Cancellation fee | No |

| Chargeback fee | $15-0 |

| Hidden fees | / |

| PayPal Standard | |

|---|---|

| Transaction fee | Flat 2.9% + $0.3 |

| Negotiable rates | No |

| Monthly fee | None |

| Setup fee | None |

| Contract | No |

| Cancellation fee | No |

| Chargeback fee | Varies ($20 for Canadian) |

| Hidden fees | / |

| PayPal Pro | |

|---|---|

| Transaction fee | Flat 2.9% + $0.3 |

| Negotiable rates | Yes |

| Monthly fee | $35 (+HST) |

| Setup fee | None |

| Contract | No |

| Cancellation fee | No |

| Chargeback fee | Varies ($20 for Canadian) |

| Hidden fees | / |

| Bambora | |

|---|---|

| Transaction fee | Flat 2.8% + $0.3 |

| Negotiable rates | Yes Over $5million/year |

| Monthly fee | $25 |

| Setup fee | $49 |

| Contract | Month to month |

| Cancellation fee | No |

| Chargeback fee | $20 |

| Hidden fees | / |

| Moneris | |

|---|---|

| Transaction fee | Quote-Based(~ 1.6% + $0.05) |

| Negotiable rates | Yes |

| Monthly fee | Yes, varies (~$40 +HST) |

| Setup fee | Yes, varies (~$150 +HST) |

| Contract | Quote-Based |

| Cancellation fee | Yes |

| Chargeback fee | ~$25 |

| Hidden fees | Yes |

Other payment processors available in Canada

Beyond Stripe, PayPal, Bambora, and Moneris here are some of the other payment processors available in Canada:

- Square

- Authorize.net

- PSi Gate

How to choose a payment processor

Now that you have a clear image of payment processing options available, what they offer and how much they cost, let me show you how to make the decision on which one is the right for you.

Your choice will probably largely depend on the cost, so let’s break it down into three tiers…

Best payment processor if you’re processing under $10K/month

With low processing volumes (under $10K/month) your costs will be largely dominated by fixed fees. That’s why you want to avoid any processors that charge a monthly fee.

You also want to avoid long approval periods, contracts and confusing pricing plans (like Bambora and Moneris).

Fixed fees, quick setup and no commitment will give you peace of mind when starting your e-comm business.

The choice narrows down to Stripe and PayPal.

Let’s do some quick math:

For example, if your average sale is at $100 and you make around 50 transactions each month, it’s…

Stripe/PayPal Standard: $100 x 2.9% + $0.3 = $3.2 per transaction

50 transactions x $3.2 = $160 per month

PayPal Pro: $100 x 2.9% + $0.3 = $3.2 per transaction

50 transactions x $3.2 + $35 monthly fee = $195 per month

| Stripe | PayPal Standard | PayPal Pro | |

|---|---|---|---|

| Cost per transaction | $3.2 | $3.2 | $3.2 |

| Monthly processing costs | $160 | $160 | $195 |

In our example, Stripe will cost $3.2 per transaction, adding up to a monthly processing cost of $160.

| PayPal Standard | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $160 |

| PayPal Pro | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $195 |

PayPal Standard will cost you the same as Stripe for domestic transactions. PayPal Pro, with its $35 monthly fee would end up costing you around 22% more.

However, since PayPal Standard redirects customers off your site, your best option is Stripe.

Also note that as your revenue increases and gets closer to the 10K mark, the margin between PayPal Pro and Stripe narrows to less than 10%.

Best payment processor if your processing between $10-100K/month

When processing between $10-100K monthly, the fixed monthly fee becomes less of a factor.

For example, if your average sale remains $100 but you process around $35K/month (350 transactions):

Stripe/PayPal Standard: 350 transactions x $3.2 per transaction = $1120 per month

PayPal Pro: 350 transactions x $3.2 per transaction + $35 monthly fee = $1155 per month

So, the difference is now is around 3% and going down as your revenue increases.

At this stage, it makes sense to throw in Bambora Blended plan into the mix (2.8% + $0.3 per transaction and $25 monthly fee).

Bambora: $100 x 2.8% + $0.3 = $3.1 per transaction

350 transactions x $3.1 + $25 monthly fee = $1110 per month

| Stripe | PayPal Standard | PayPal Pro | Bambora | |

|---|---|---|---|---|

| Cost per transaction | $3.2 | $3.2 | $3.2 | $3.1 |

| Monthly processing costs | $1120 | $1120 | $1155 | $1110 |

| Stripe | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $1120 |

| PayPal Standard | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $1120 |

| PayPal Pro | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $1155 |

| Bambora | |

|---|---|

| Cost per transaction | $3.1 |

| Monthly processing costs | $1110 |

More volume also means you could start thinking long term. That is, if you reach higher revenues in the future, what processors you can negotiate better rates with.

Both Stripe and PayPal allow you to negotiate rates at higher volumes. However, your mileage will vary depending on your haggling skills.

On the other side, Bambora requires you to process at least $5 million annually to be eligible for lower rates (Interchange Plus), which is just one more thing to consider.

Best payment processor if your processing over $100K/month

Beyond $100K, Stripe and PayPal start making less sense. Even if you negotiate lower rates, they’re typically always going to be higher than what you can get from Bambora and Moneris.

Once you exceed $100K per month, Bambora (Interchange Plus) and Moneris are your best bet.

They will allow you to process credit cards at a flat rate above interchange which depends on your volume. You can expect to pay anywhere between 1.6 -2.3% on average in transaction fees for Visa and Mastercard.

The rates for accepting American Express get around 2%, as opposed to Stripe >2.9% and PayPal 3.5%. Debit cards are the lowest at around 0.5%.

For example, if you average $100 per sale and reach $500K/month (5K transactions), that is…

Stripe/PayPal: $100 x 2.9% + $0.3 = $3.2 per transaction

5K transactions x $3.2 = $16K per month

Bambora/Moneris : $100 x 2% (rough estimate) = $2 per transaction

5K transactions x $2 = $10K per month

| Stripe/PayPal | Bambora/Moneris | |

|---|---|---|

| Cost per transaction | $3.2 | $2 |

| Monthly processing costs | $16K | $10K |

| Stripe/PayPal | |

|---|---|

| Cost per transaction | $3.2 |

| Monthly processing costs | $16K |

| Bambora/Moneris | |

|---|---|

| Cost per transaction | $2 |

| Monthly processing costs | $10K |

That’s 6K saved per month ($72K annually), just by getting a better transaction rate!

The rates will largely depend on your yearly volume and your overall processing cost on the ability to negotiate and waive unnecessary fees.

At this point the monthly fees are barely noticeable, so you can opt-in for contracts with these two companies and try to reduce your rates to a minimum.

Other things to consider when choosing a payment processor for e-commerce

Transaction rates are one of the biggest factors, but far from being the only one to consider.

The following are also some of the things you need to account for when choosing your payment processor.

Are you just starting out with e-commerce

If you’re just starting out, the simplicity of Stripe and PayPal is unbeatable.

You get a flat transaction fee, so your costs are clear and predictable.

With Stripe and PayPal Standard, there are no overheads like monthly fees, no upfront setup costs, and no long-term commitment. These are all key when you’re just starting out with e-commerce because you want to keep your fixed costs to a minimum.

So, the go for Stripe or PayPal and you can always make a switch down the line once your business is more stable and you get more data to work with.

Keep in mind that payment methods your customers prefer

One of the most important things to consider is who are your customers are and which payment methods they prefer.

For example, if you’re selling B2B your customers are likely using American Express.

That means you need to look for the best AMEX rates.

PayPal won’t be a good option for this (3.5% fee). You might want to go for Moneris or Stripe (if you’re processing low volumes) instead.

So far, for AMEX the best rates we’ve seen come from Moneris at only 2% + $0.05.

On the other hand, if you’re selling B2C you must consider that many consumers prefer to use PayPal to pay for their purchases. It’s super convenient, people don’t have to dig through their wallet for their card and this can help boost conversions.

So, you must include PayPal in the mix.

Go for PayPal Pro to accept both PayPal funds and cards on your own website.

Or if you want to use some other processor, consider PayPal Payments Standard on top of your current checkout.

Adding PayPal as an additional payment option will help you grab those customers that don’t want to give you their credit card.

Do you only sell online or you have a physical store as well

For pure e-commerce stores, you can start with Stripe or PayPal.

On the other hand, if you run both a physical and online store, you also need POS hardware.

PayPal does offer a Virtual Terminal to turn your phone into a simple card reader. However, the rates are not that great.

- Domestic 3.1% + $0.3

- US 3.9% + $0.3

- International 4.1% + fixed fee depending on the country

- 3.5% for AMEX

Moneris offers professional POS equipment such as card terminals, PIN pads, iPads, etc.

They do require you to fork up additional rental fees, but for large volume retailers, this is a normal cost of doing business.

Consider if you’re selling only domestic or international

Think about where you’re selling, as transaction rates can vary largely between domestic (Canada) and international payments.

PayPal charges 3.7% + $0.3 for US and 3.9% + fixed fee (depending on country) for international payments.

Stripe charges an extra 0.6% for all payments outside Canada. This comes to comes to 3.5% + $0.3 per international sale.

Just do be aware that Stripe charges an extra 2% fee if the payment requires a currency conversion. PayPal’s currency conversion fee is a minimum of 3.5% for Canadian or U.S. dollars or a minimum of 4.0% for all other currencies.

So, if you’re making a bulk of your sales outside Canada, make sure to shop around for the best international rates.

And in this case, that might be Stripe.

Which currencies do you accept

If you plan to accept multiple currencies, such as CAD and USD for example, your best choice would be Stripe or PayPal. Both companies allow you to accept multiple currencies using a single account.

On the other hand, Moneris and Bambora will require you to set up a different account for each currency. That means you’ll have to pay again for setup, double monthly fee, etc.

This can be negotiated, but for new and small businesses, it’s better off opting for Stripe or PayPal.

Watch out for hidden fees

Some payment processors are riddled with hidden fees and if you don’t look at the fine print of your contract you may be in for a nasty surprise.

Hidden fees are common with processors that require a contract commitment, such as Moneris and Bambora.

These can include setup fees, PCI compliance fees, deposit fees, equipment rental, early termination fees, etc. Many of these are completely unnecessary and just pose a burden for your business.

Luckily, some of these hidden add-ons and fees can be waived if you’re good at negotiation and you know what you’re doing.

Sales agents are very good at convincing you that you need everything, so do your research and be persistent.

Don’t forget security and PCI compliance

Regardless of which processor you go for, the payments are secure only if your website is secure. Especially if you’re hosting the checkout on your own domain.

PCI (Payment Card Industry) security standards apply to any e-commerce site that handles payments from credit/debit cards. This means that your site needs to be secure and PCI compliant to avoid fines and penalties.

If you don’t have a website, make sure your web development agency can hook you up with a secure e-commerce website.

At StableWP, all of our websites are secure with top of the line 128-bit SSL certificates and build in compliance with the PCI standard. This protects our clients from hacking and stealing their customers’ sensitive information such as identity and payment credentials.

Also, if you have an existing e-commerce website and you’re not sure if you’re PCI compliant and protected by the latest security features, contact us for a free website audit.

Payment processor FAQ

Here are some of the most common payment processing questions answered.

What is a merchant account

A merchant account is where the funds go when successfully approved and captured after an e-commerce transaction.

You need a merchant account to accept payments online. You can later transfer funds from your merchant account into your bank account for further use.

Merchant accounts and payment gateways can be offered separately, or they can be combined in a single solution.

What is the difference between a payment processor and a payment gateway

A payment gateway is a service that helps merchants accept payments online, which is essential for e-commerce. It usually comes as a plugin integrated into your e-commerce platform.

A payment processor, on the other hand, communicates with the customer’s card issuer. When it confirms that there are sufficient funds to cover the purchase, the transaction is approved. Then the funds are transferred from the customer’s account to your merchant account.

What is an Interchange fee

Interchange is a fee that the credit/debit card issuers charge for every transaction.

Every time your customers pay with a credit or debit card, their card issuer will charge a percentage plus a fixed fee. This can vary by card type (standard, premium, corporate, etc.), transaction type (chip, swipe, e-commerce, etc.) and the business type.

In addition, the credit card association (Visa, MasterCard, etc.) adds on a fee, called an assessment.

Note that people usually lump the two together as the “interchange fee.”

What is the network assessment fee

An assessment fee is an amount that card brands (VISA, MasterCard, AMEX, etc.) charge for each transaction.

For example, the assessment rate for Visa is 0.13% for credit cards and 0.11% for debit cards. If a cardholder makes a $100 purchase using a Visa credit or debit card, then the Visa card association will receive $0.13 or $0.11 in assessment fees depending on the card type.

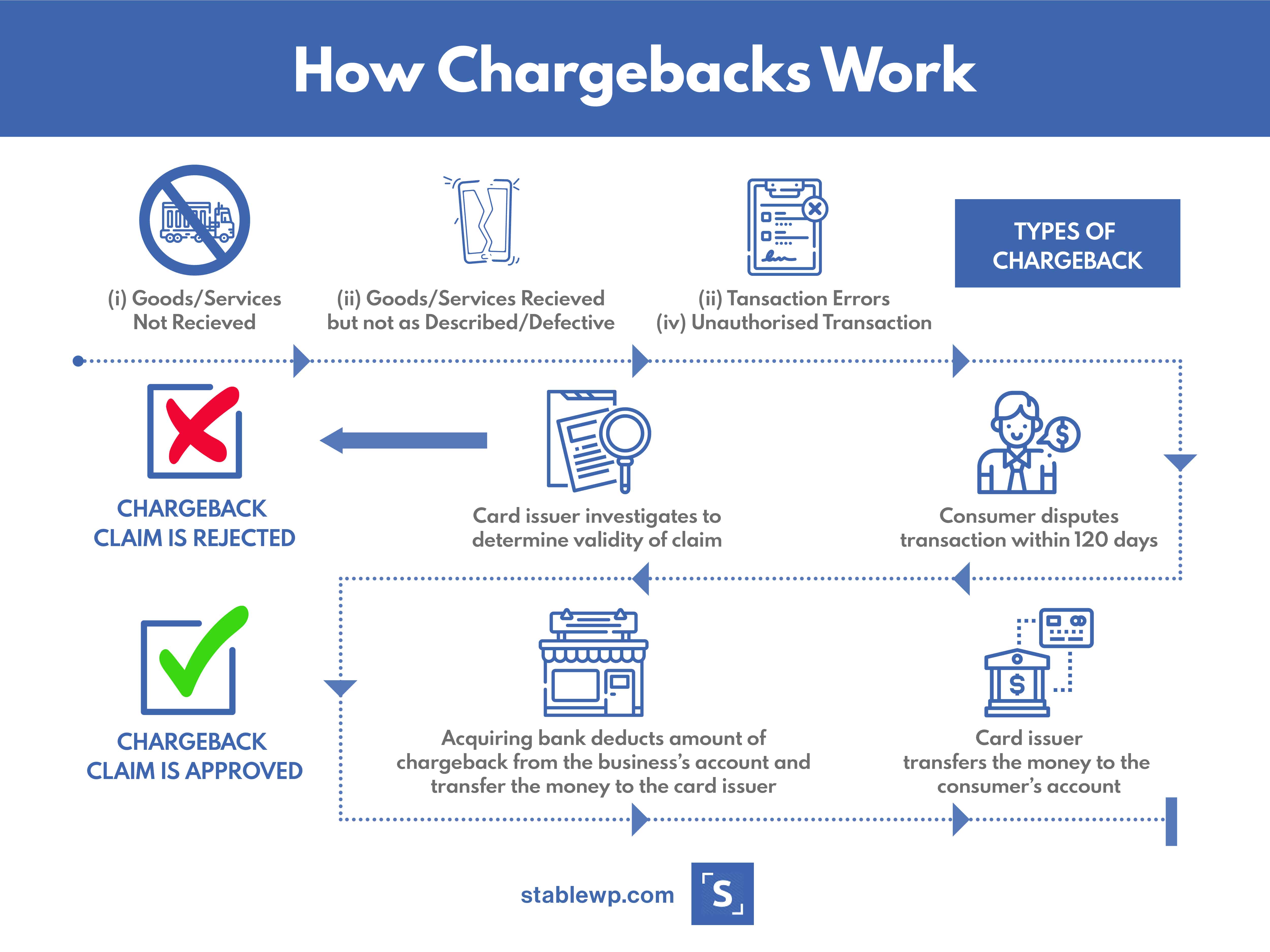

What is a chargeback

A chargeback is a dispute of a purchase that has already been charged to an account that can result in a return of funds.

Most payment processors charge a chargeback fee which stands around $15-25CAD in Canada.

What is PCI compliance

PCI compliance is a set of standards enacted by the credit card community to ensure that all credit card transactions are secure.

The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that accept, process, store or transmit credit card information maintain a secure environment.

This is especially important for e-commerce businesses.

In order for your online store to be PCI compliant, you must follow a set of guidelines in order to process credit cards on your website or face fines or penalties set forth by your credit card processor.

Can I use multiple payment processors at the same time

Yes.

There’s no limit to how many processors you can addon your e-commerce store.

One of the most common combinations is to:

- Use Stripe to process credit/debit cards because of its simplicity, no monthly fees, and predictable rates, and

- PayPal Standard to process payments from PayPal and others who might not want to give you their card information. Users can log in with only their PayPal account to reduce friction and cart abandonment.

Key Takeaway

Choosing the payment processor for your e-commerce is one of the most important decisions.

Shop around for the solution that fits your needs, with decent rates and minimum overheads. It comes down to your sales volume, who your customers are and your ability to negotiate.

For new and small online businesses Stripe and PayPal make the most sense.

With processing higher volumes, go for Bambora or Moneris as they can offer much better rates.

And if you need any help setting up your e-commerce leave a comment or reach out directly.

Good luck with your new e-comm!

[do_widget id=custom_html-25][/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]